Getting out of debt isn’t just about willpower—it’s about strategy. Whether you’re facing high-interest credit cards, installment loans, or simply want to regain control of your finances, a clear, step-by-step approach can turn chaos into progress.

This guide walks you through practical methods to assess your financial baseline, build a goal-focused budget, and choose the smartest repayment path for your situation.

Assess Your Financial Baseline

Track inflows and outflows to avoid guesswork. Record wages, freelance payments, and irregular income in a spreadsheet or budgeting app, categorizing expenses—housing, transport, subscriptions, discretionary purchases—to pinpoint hidden cash drains.

List all debts, noting balances, annual percentage rates, minimum payments, and due dates. Gather credit card statements from all issuers and installment contracts for phones, appliances, or personal loans.

Calculate total monthly interest to see why balances barely change when only minimums are paid. Finally, review credit card transactions for spending patterns that can be trimmed or shifted to cheaper options, like interest-free promotional plans.

Build a Goal-Driven Budget

Allocate funds first to essential costs—housing, utilities, groceries, insurance—since missed payments incur immediate penalties. Dedicate the next part of income to debt reduction, exceeding the combined minimums.

Choose between the debt snowball (paying smallest balances first) and debt avalanche (targeting highest rate accounts).

Whichever method you prefer, automate transfers on payday to protect progress. Keep a modest emergency buffer to avoid new borrowing for unexpected expenses.

Optimize Installment Accounts

Log each due date in a calendar app with reminders three days prior to avoid late fees. Assess balances against market offers; refinancing or balance transfers may reduce costs, especially during promotional zero-rate periods lasting twelve months.

Contact lenders for term extensions or interest reductions if income volatility affects payments; many adjust terms to maintain account performance instead of risking default.

When buying large items, compare retailer financing with traditional bank loans, focusing on total cost rather than the monthly payment shown in ads.

Control Credit Card Use

Set personal spending caps below the issuer’s limit since lower utilization improves credit scores and reduces stress. Enable real-time alerts for every transaction to reduce impulse buys.

Pay the full statement balance by the due date; avoiding interest is like earning money. If full payment isn’t feasible, schedule bi-weekly payments aligned with paydays to lower average daily balance and interest charges.

For high-rate cards, consider a consolidation loan or zero-percent balance transfer, weighing fees against savings. If cash flow issues are temporary, negotiate with issuers about hardship programs that may reduce rates or waive fees for months.

Prioritize Debt Repayment

Begin by identifying any delinquent or near-delinquent accounts because late statuses quickly damage credit and may involve legal action.

Next, review secured debts such as auto loans or mortgages; protect these to avoid repossession or foreclosure. For unsecured balances, decide whether accelerating high-interest accounts or small-balance accounts will keep motivation stronger for you.

Use a free online debt paydown calculator to test scenarios and pick a path that your cash flow can sustain without resorting to new borrowing.

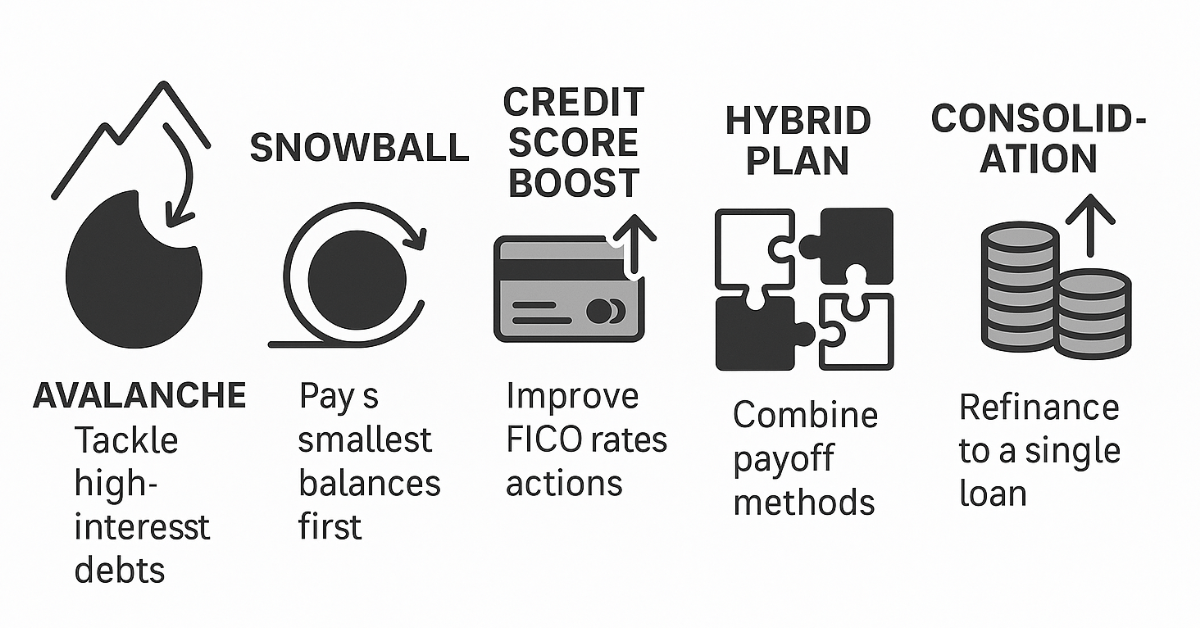

Five Payoff Strategies for 2025

Each method below offers a structured route to elimination; select one or combine several to match personal circumstances.

- Avalanche Method — Funnel every extra unit of currency toward the account with the highest rate while maintaining minimums elsewhere, saving the most on interest over time.

- Snowball Method — Focus on the smallest balance first to secure quick psychological victories that build momentum for larger challenges.

- Credit-Score Boost Approach — Lower cards with utilization above thirty percent to lift credit scores rapidly, unlocking cheaper financing options.

- Hybrid Plan — Mix tactics by clearing any account in collections immediately, then alternate between avalanche and snowball steps to keep both savings and motivation high.

- Consolidation Route — Replace several high-APR balances with one lower-rate loan or balance transfer card, simplifying administration and often shortening payoff time, provided new spending is curtailed.

When Professional or Relief Options Make Sense

Reach out to creditors early to request hardship variations rather than waiting for missed payments, since issuers favor proactive customers worldwide.

Nonprofit credit-counseling agencies create debt management plans that consolidate unsecured debt into a single monthly payment, often at a lower interest rate. In severe cases, evaluate debt settlement firms cautiously; their fees and potential credit damage may outweigh benefits unless insolvency is imminent.

Bankruptcy is a last resort, but Chapter 7 or 13 can offer a fresh start when income cannot meet obligations. Consult a licensed attorney for jurisdiction-specific impacts, including asset protection and borrowing limits.

Compare Popular Consolidation Pathways

Choosing the right consolidation tool depends on credit profile, asset ownership, and urgency.

- 0 Percent Balance Transfer Card

- Introductory windows of fifteen to eighteen months allow interest-free progress, provided the transferred sum is cleared before the promotional period ends.

- Upfront transfer fees of two to three percent must be weighed against saved interest.

- Fixed-Rate Personal Loan

- Predictable monthly installments simplify budgeting and often carry rates below those of revolving credit, especially for applicants with strong scores.

- Origination charges or long repayment terms can erode benefits if not analyzed carefully.

- Home Equity Loan or Line of Credit

- Lower secured rates reduce costs significantly when solid equity exists and property markets remain steady.

- Default risk shifts from unsecured credit toward potential foreclosure, raising stakes considerably.

- Debt Management Plan through Counseling Agency

- Consolidates unsecured balances into a three-to-five-year structured program often accompanied by interest concessions.

- Access to new credit may be restricted until the program completes.

Reduce Living Costs to Accelerate Results

Negotiate service contracts globally—mobile, broadband, insurance—once a year, leveraging competitor offers to secure lower rates.

Replace costly entertainment subscriptions with free or ad-supported alternatives and prioritize community events or public parks over ticketed venues.

Batch-cook meals and embrace discount grocery cycles to curb dining-out costs, and review energy usage to shave utility bills. Any savings should transfer instantly into the payment account, preventing lifestyle creep from absorbing gains.

Quick Answers to Common Credit Card Questions

Practical knowledge resolves uncertainty and supports confident decision-making.

- Missing a Minimum Payment triggers an arrears status, prompts issuer contact, and can lead to default notices after several cycles, so communicate immediately to arrange temporary adjustments.

- Negotiating a Partial Settlement may close an account for less than owed; ensure written confirmation and understand that credit reports will reflect the settled status for several years.

- Shared Card Usage on an account in one name keeps legal responsibility with the primary cardholder, so authorize additional users only when repayment discipline is unquestioned.

- Persistent Debt Definition refers to situations where interest and fees paid over eighteen months exceed principal reduction; issuers must alert users and may propose higher minimums.

- Balance transfers can be helpful when a clear plan exists to pay off the debt within the zero-rate period; however, fees and post-promo rates can make complacency expensive.

Keep Progress Visible and Sustainable

Update a payoff tracker every payday, plotting declining balances on a simple line graph or coloring segments of a debt thermometer.

Celebrate reaching major milestones, such as paying off the first card or passing the halfway mark, but reward yourself with experiences that do not add debt.

Revisit the budget quarterly to redirect any income increases straight toward repayment goals, maintaining the momentum that eventually carries every balance to zero. Continual tracking ensures that detours remain temporary and that the finish line stays clearly in view.

Conclusion

Debt freedom rarely happens overnight, but it does happen when your actions stay consistent and your strategy adapts to real life.

From budgeting smarter to choosing the right payoff method and seeking support when needed, every step you take builds momentum.

Track your progress visibly, cut costs where possible, and keep your focus on a future where every payment moves you forward, not just keeps you afloat.